お店で受け取る

お店で受け取る

(送料無料)

配送する

配送する

納期目安:

2025.10.27 22:22頃のお届け予定です。

決済方法が、クレジット、代金引換の場合に限ります。その他の決済方法の場合はこちらをご確認ください。

※土・日・祝日の注文の場合や在庫状況によって、商品のお届けにお時間をいただく場合がございます。

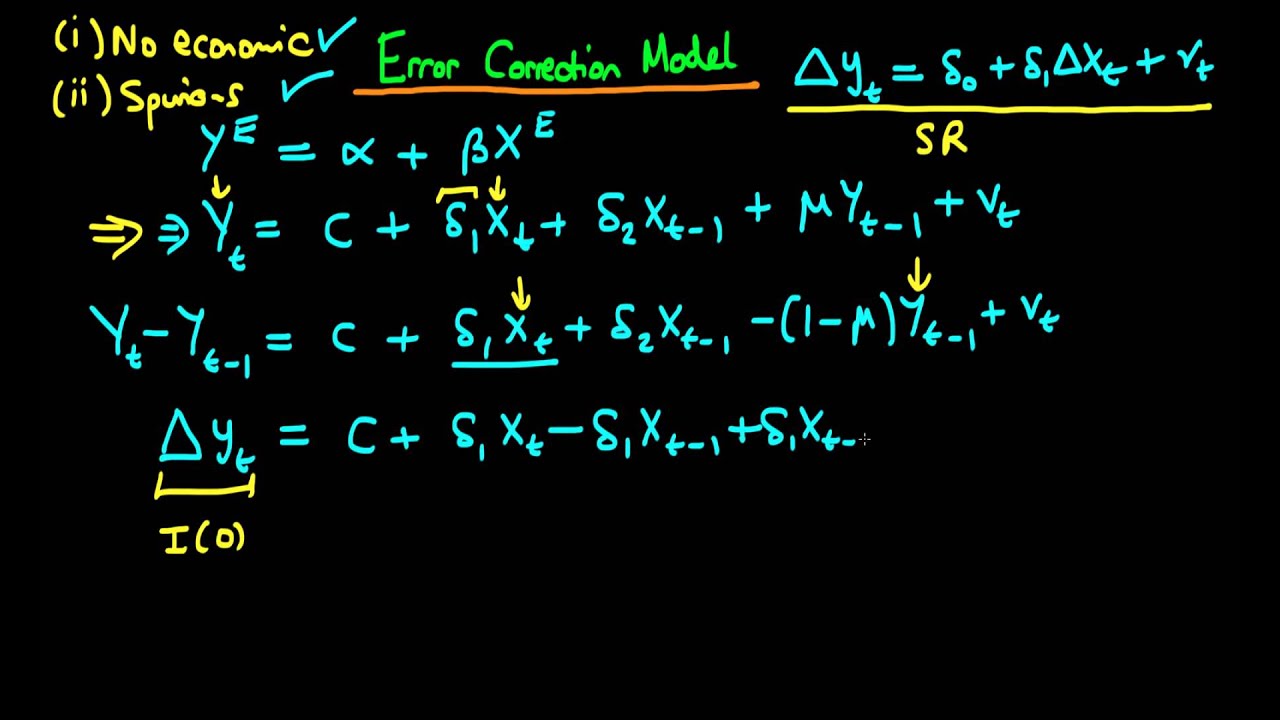

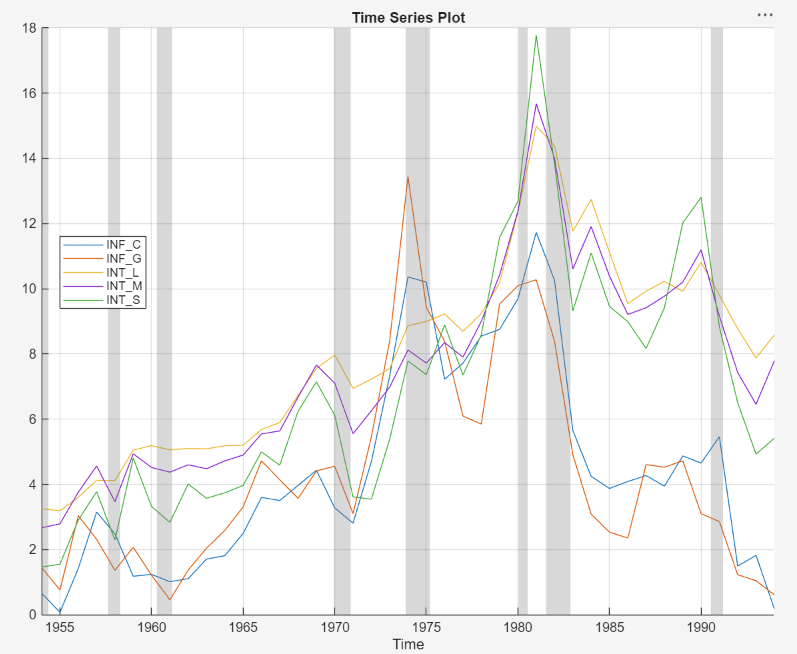

ビジネス・経済 Co-Integration, Error-Correction, Econo Econometrics - Vector Error Correction Model: Johansen Testの詳細情報

Econometrics - Vector Error Correction Model: Johansen Test。16.3 Cointegration | Introduction to Econometrics with R。VECM Estimation and Interpretation - SPUR ECONOMICS。非定常データの計量経済学分析に関する理論と実践的手法を網羅した専門書。Vector Error Correction Model Configuration & Analysis | by。- タイトル: Co-Integration, Error-Correction, and the Econometric Analysis of Non-Stationary Data- 著者: Anindya Banerjee, Juan Dolado, John W. Galbraith, David F. Hendry- シリーズ名: Advanced Texts in Econometrics- 内容: 非定常データの計量経済学分析に関する理論と実践的手法- 言語: 英語ご覧いただきありがとうございます。朝日新聞 縮刷版 2009年(平成21年) 7〜12月 6冊セット。

ベストセラーランキングです

この商品を見た人はこんな商品も見ています

-

マイストア在庫: 3178税込9,164円

マイストア在庫: 3178税込9,164円 -

マイストア在庫: 1610税込9,570円

マイストア在庫: 1610税込9,570円 -

マイストア在庫: 3481税込6,960円

マイストア在庫: 3481税込6,960円 -

マイストア在庫: 3531税込19,390円

マイストア在庫: 3531税込19,390円 -

マイストア在庫: 3909税込6,666円

マイストア在庫: 3909税込6,666円

近くの売り場の商品

カスタマーレビュー

オススメ度 4.1点

現在、4441件のレビューが投稿されています。